Background

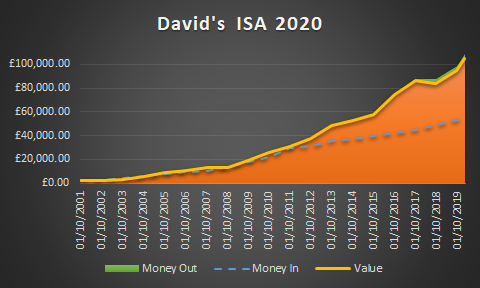

21/02/2020– This is my Stocks & Shares ISA consisting of over 30 managed funds. I charge the ISA 3% on each contribution plus 0.5% per annum of fund value for an “investment performance review”. The yellow line shows value after costs and the blue dotted line shows gross contributions. Green block shows money taken out. Everyone’s ISA will perform differently depending on funds held, amount invested, timescale and charges. £350 per month goes in (at the start it was only £50pm.) I sometimes make additional, lump sum contributions and have withdrawn money in the past.

Commentary

Markets rose again at the end of 2019 on the back of improving trade relations between the US and China. In the UK, greater clarity over Brexit also benefitted investors. This growth may take a hit if interest rates rise and/or governments curb spending but there is no sign of this happening in the immediate future.

ISA benefits

The 2019/2020 UK ISA allowance is £20,000. Consider using up as much of this as possible before the 5th April 2020 deadline. If you do not wish to invest the full amount, you can fill up any unused allowance with a Cash ISA

The obvious advantage of an ISA is the fund is invested in a virtually tax free environment. If you are a non tax payer, have capital gains below the annual allowance, receive less than £2,000 p.a. in dividends, or make a loss – these may not seem like advantages. However, it may still be worth placing money into an ISA to protect you from future tax charges and admin. ISA money does not need to be included in a tax return..

Warnings & Caveats

This investment suits me but may not suit you. It’s value can fall, so can the amount of income it produces. I never recommend you invest in anything without first seeking proper regulated advice – unless, of course, you fully understand the risks and have the capacity to accept the loss.

If you have your own ISA, it may perform differently for the reasons given above.

Please note, I also keep a Cash ISA going for Emergencies. Returns are not great at present but the capital value should be safe.

I can’t predict the future..