Background

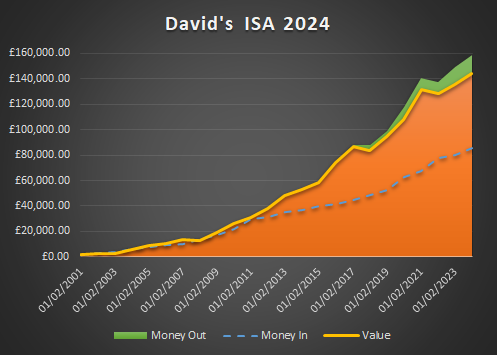

07/02/2024 – This is my Stocks & Shares ISA consisting of over 30 managed funds. I charge the ISA 0.5% per annum of fund value for an investment performance review. The yellow line shows value after costs and the blue dotted line shows gross contributions. Green block shows money taken out. Everyone’s ISA will perform differently depending on funds held, amount invested, timescale and charges. £500 per month goes in (at the start it was only £50pm.) I sometimes make additional, lump sum contributions and have withdrawn money in the past.

Commentary

Inflation has caused central banks to raise interest rates in the last couple of years. This, in turn, has made investors nervous about economic growth prospects and many have put their money into cash deposits where risk free returns are better than they have been for over 10 years. The world is also aware of burgeoning global conflicts and changing supply chains. This upheaval tends to make companies and investors cautious and affects growth. One area of outperformance has been a relatively small number of U.S. “tech” stocks and the growth of AI.

Although the portfolio has only grown about 2% on the year, I am confident the assets it holds will eventually catch up with inflation. There is always a risk too many old people are trying to sell their investments while not enough young people want to buy them. This would cause a drop in value. However, global population levels still appear to be rising…

ISA benefits

The 2023/2024 UK ISA allowance is £20,000. Consider using up as much of this as possible before the 5th April 2024 deadline. If you do not wish to invest the full amount, you can fill up any unused allowance with a Cash ISA.

The obvious advantage of an ISA is the fund is invested in a virtually tax free environment. If you are a non tax payer, have capital gains below the annual allowance, receive less than £1,000* p.a. in dividends, or make a loss – these may not seem like advantages. However, it may still be worth placing money into an ISA to protect you from future tax charges and admin. ISA money does not need to be included in a tax return..

* this figure is due to drop to £500 next tax year increasing potential ISA advantages.

Compare with last year’s ISA graph

Warnings & Caveats

This investment suits me but may not suit you. It’s value can fall, so can the amount of income it produces. I never recommend you invest in anything without first seeking proper regulated advice – unless, of course, you fully understand the risks and have the capacity to accept the loss.

If you have your own ISA, it may perform differently for the reasons given above.

ISAs are not much use against Inheritance tax as they form part of your estate on death. However, spouses can “inherit” each other’s ISA fund value as an allowance

Please note, I also keep a Cash ISA going for Emergencies. Capital value should be safe from volatility. Cash returns have improved in the last couple of years.

I can’t predict the future..